Is It Time to Ditch Your Cash ISA?

Since their introduction in 1999, the Individual Savings Account (ISA) has been a huge success. Replacing the ‘Personal Equity Plan’ (PEP) and ‘Tax-Exempt Special Savings Account’ (TESSA), in essence, an ISA is a tax-free savings and investment plan allowing individuals to grow their money without paying any income tax or capital gains tax.

Since their introduction, the amount invested in ISAs has mushroomed as people warmed to the tax-free status they enjoyed as well as (in most cases) retaining complete access to their money (unlike investing in a pension).

Up until recently, there was a distinction between ‘cash ISA’s’ and ‘stocks and shares ISAs’. The rules have since been merged and the ISA family has grown to include the ‘Help-to-buy ISA’, ‘Lifetime ISA’, ‘Innovative Finance ISA’, ‘Junior ISA’, ‘Flexible ISA’ and ‘Inheritance ISA’. Without going into the technicalities of the differences, many people still understand that they can use their ISA for cash (effectively a bank account) or an ‘invested’ ISA that uses funds or stocks to provide an investment return.

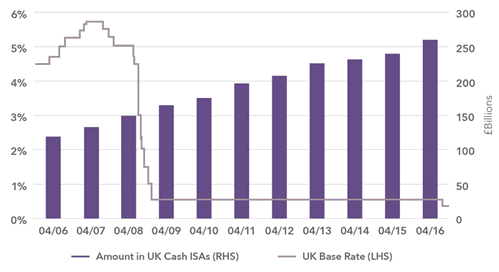

Cash ISAs became incredibly popular early this century and their popularity shows no signs of abating. Today, there is more than £250bn invested in cash ISAs in the UK. In early 2001, some cash ISAs were offering a rate of 7.25% with investors able to contribute up to £3,000 a year. A fully funded ISA would earn £217 a year – a healthy return with almost no risk at all.

Today, those rates seem a world away. Even the best instant access ISAs are now giving savers less than 1% a year. And that’s the best ones – the worst are barely paying any interest at all. This means the very best return on that same £3,000 is now around £25 a year in interest.

Inflation destroys returns

Today, inflation in the UK stands at 1.8% meaning even the best cash ISA will be likely to lose money in real terms. With the recent fall in Sterling against other currencies, inflation expectations are in the 3-4% range over the next couple of years. If ISA rates don’t pick up (and there is little sign they will), savers could be losing 2-3% a year. Someone who had amassed £30,000 in cash ISAs could be losing £1,000 a year just by holding money in a cash ISA.

Savings versus investing

Most people are comfortable with ‘saving’. Risk-free, simple and easy to understand. ‘Investing’ is seen as complicated, risky and difficult – but it needn’t be. Everyone should have some savings. Savings are crucial to pay for unforeseen emergencies like losing your job or if you are likely to need your money in the short term (less than 5 years). For those who are putting their money away for the longer-term, they should probably be ‘investing’, not ‘saving’.

Investment markets rise and fall and aren’t right for everyone, but the reality is that the only real way to make your money grow (or even stand still) in an ISA today is to invest, not save.

If you are unsure about whether you should invest and how best to do this, you are best off speaking to a chartered financial planner or other independent expert.

So what are your options?

ISA’s can be consolidated and transferred into an alternative ISA at any time. No longer are ‘cash ISA’s and ‘stocks and shares ISAs’ kept separate. This means you can invest when you need to and save when appropriate.

One option is to transfer some of your cash ISAs into investment funds. You don’t need to take on a massive around of risk – just enough to get your money growing. A financial planner can help assess your attitude to risk and create a diversified portfolio that should minimise the downside as well as providing growth when investment markets rise. Depending on the amount of risk you are willing to take, an average annual return of 5%-8% is realistic, but remember, you will have times when your investment falls in value so you need to always think long-term.

Another option is an ‘Innovative finance ISA’. This means you effectively lend your money to borrowers through what is known as ‘peer-to-peer (P2P) lending’. This is a relatively new form of financial product so the market is still developing and risks being assessed. While not risk-free, the risk may be lower than putting your money in some investment funds, with returns likely to be in the 4%-6% range. You can still lose money but, as you lend to a wide range of borrowers, the risks of significant defaults (losses to you) are minimal.

Get an ISA boost

Whatever you invest in – cash, investment funds or P2P lending, from April 2017, many people will be able to take advantage of the new ‘Lifetime ISA’ (LISA). This type of ISA comes with a free government top-up (free money!) but also comes with some significant health warnings; it and may actually end up costing you money, not making you money. As usual, the devil is in the detail and the pros and cons need to be weighed up carefully.

Wrapping up

ISAs are a great way to save and invest, but the range of different ISAs and different investment options can be confusing. Seeking expert independent advice can help you clarify your options and work out what is best for you. If you have savings sat in a cash ISA, there has never been a better time to take a long hard look at it. Think carefully about what you are trying to achieve and understand that holding significant amounts in cash for the long-term is unlikely to be a good strategy.

Your cash ISA is almost certainly losing you money. That is not in question. The question is – what are you going to do about it? Talk to an independent financial planner and discuss your options. Don’t watch your money go down the drain. Take action now to make your money work as hard as you do.

If you want to talk through your ISA options, please contact us to arrange a free consultation.

NorthStar Insights

Stay right up-to-date with the latest financial news, get expert insight and analysis and exclusive special offers to help you make the most of your money.

NorthStar Insights is the free email newsletter enjoyed by over 3,000 people across the UK. Subscribe now to never miss another update.

Latest Articles

It’s Never Too Late: Seven Essential Strategies to Get Your Retirement Plans Back on Track 4 August 2026

It’s Never Too Late: Seven Essential Strategies to Get Your Retirement Plans Back on Track 4 August 2026- Home Bias: Why Many British Investors Have Too Much Money in UK Equities 14 July 2026

Digital Ghosts: Don’t Let Your Online Finances Haunt Your Family After You’re Gone 23 June 2026

Digital Ghosts: Don’t Let Your Online Finances Haunt Your Family After You’re Gone 23 June 2026 What the World Cup Can Teach Us About Financial Planning 2 June 2026

What the World Cup Can Teach Us About Financial Planning 2 June 2026 Raising Money-Smart Kids: Essential Tips for Financial Education at Every Age 12 May 2026

Raising Money-Smart Kids: Essential Tips for Financial Education at Every Age 12 May 2026 The Stranger in Your Mirror: Why Your Brain Can’t Connect With Your Future Self (And How Financial Forecasting Can Help) 21 April 2026

The Stranger in Your Mirror: Why Your Brain Can’t Connect With Your Future Self (And How Financial Forecasting Can Help) 21 April 2026 Are Your Pensions Fit for Purpose? The Eight Warning Signs to Watch Out For 30 March 2026

Are Your Pensions Fit for Purpose? The Eight Warning Signs to Watch Out For 30 March 2026- Twenty Simple Ways to Give Your Finances a Thorough Spring Clean 10 March 2026

- How to Manage Your Parents’ Money Through Later Life 17 February 2026

- Don’t Be a Financial Dinosaur: Ten Outdated Money Habits to Ditch Today 27 January 2026

- Revealed: The Biggest Retirement Regrets and How to Make Sure You Avoid Them 6 January 2026

- Caught in the Middle: Essential Financial Strategies for the Sandwich Generation 16 December 2025

Disclaimer

The content of this article is for information purposes only and does not constitute a personal financial recommendation. You should always speak to a regulated financial planner before taking financial advice. This article is intended for UK residents only. All information correct at time of publication.

Tag Cloud

Awards, Accreditations & Trade Associations

NorthStar is proud to be a member of the leading financial planning trade associations. Through a continued commitment to adhere to the highest professional standards and deliver exceptional service, NorthStar has received a number of awards and professional accreditations.