Are You Ready for the Savings Crunch?

Years ago we had the credit crunch – will the savings crunch be next? A double-whammy of low interest rates coupled with inflation could cause your ‘safe’ cash savings to erode. Maybe it’s time to look at some alternative strategies.

The traditional ‘hierarchy of investments’ is actually much simpler than it sounds. All it means is, there are different ways in which you can put money aside, when you want to save it and (hopefully) make it grow. Some can make your money grow faster, but will bring more risk of losing money. Others tend to bring slower growth, but will (usually) ensure that you won’t end up with less than you started with.

Things like stocks & shares fall into the bracket of ‘higher risk’ investments. At the other end of the scale we have ‘low risk’ assets such as government bonds and (of course) cash.

Cash savings are traditionally considered among the safest assets, if not the safest. You put £100 in a savings account and it earns interest – or at the very least, it continues to be worth £100.

Unfortunately, there are times when that doesn’t happen. Cash savings are subject to two opposing forces: interest on the one side, and inflation on the other. And while interest increases the number of pounds in your bank account, inflation decreases the buying power of each of those pounds. The challenge for you as a saver is to make sure the first of these horses stays ahead of the second: you want interest to outpace inflation, not the other way around.

Unfortunately, this race just hotted up.

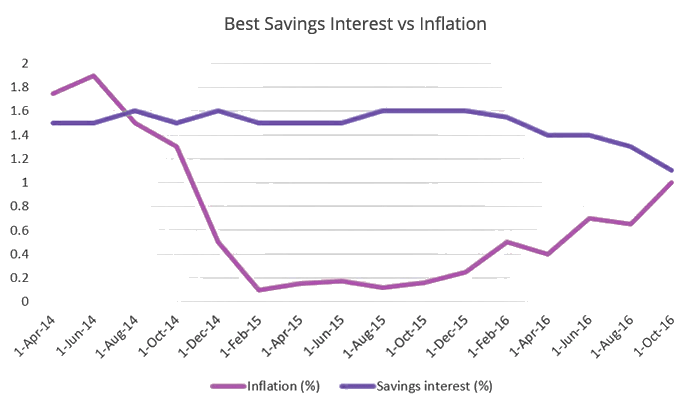

Interest versus inflation

Savers have had a difficult few years. Interest rates have been very low ever since the 2008 financial crisis, falling even lower from 2012, and the turmoil surrounding the Brexit vote caused yet another cut – just when an increase seemed to be on the cards. This made saving frustrating, but with inflation also very low it was still possible to earn small returns over time.

However, in the wake of the Brexit vote, inflation has begun to rise again. As the graph shows, savings interest on the best-value easy access accounts has managed to stay ahead of inflation since around August 2014. But the signs are that the lines will soon cross again, bringing inflation higher than the best savings interest.

The latest estimates from the Bank of England show that they expect inflation to push up towards 3% in 2017 and probably stay above their own 2% target for some time. The Bank has warned that inflation could even go as high as 4% or even 5% over the next couple of years.

With inflation likely to return with a vengeance and little sign that interest rates are due to rise any time soon, this could spell real problems for savers.

Not all savings accounts are created equal

The chart above shows the savings rates for the best accounts available but there are many that pay less interest – way less. A study done in July 2016 showed that more than 600 bank accounts were paying less than 0.3% interest so the reality for many people is that their savings have been losing money in real terms for some time – and this is only going to get worst.

When is low-risk saving risky?

Investing is about risks versus returns: the risk of losing money, weighed against the chance of earning more. Every investor from Warren Buffett downwards must tackle this balancing act. But many savers dislike the idea of any risk at all, preferring to stick exclusively to cash savings. What they may not realise is that in a high-inflation, low-interest economy, cash savings are not zero risk. On the contrary: in that environment, they are virtually guaranteed to lose you money.

Of course, a cash savings account with £1,000 in it will never show less than £1,000 if you take no money out, even in a zero-interest economy (but see the caveat below…). However, inflation at 1% will reduce its buying power to £990 in the course of single year. That’s not a huge loss, but no-one wants to discover that their carefully saved money is actually shrinking. For instance, as recently as 2011 inflation was over 5%. If you were to have £10,000 of savings at 1% interest, then 5% inflation would cost you around £400 of buying power over the year.

Now for the caveat. We said that an account with £1,000 in it would never show less than £1,000. However, this can happen in a climate of negative interest rates. If rates go so low as to be negative (as they did in Japan) then it will actually cost you money to keep savings in a bank. There are no signs yet of this happening in the UK – but we’ve had surprises before.

How to reduce risk – by taking on more

In a low-interest, high-inflation economy, the risk involved in cash savings will rise. You might not lose large sums, but some loss may be inevitable. In this situation, even the most cautious saver may want to start exploring alternative ways to save and invest. This is particularly true at times when the stock markets appear to be doing so much better than savings accounts.

But that doesn’t mean throwing caution to the winds and swapping all your cash for a bunch of shares. The secret of successful investing is to understand the nature of risk – and specifically, what ‘risk’ means for you personally.

For example, if you are saving for a time in the future (such as a child going to university in five years’ time) then a loss of a few hundred pounds in one particular year may not hinder your overall plan, so long as overall growth over the five years is positive. However, steady annual losses (or static savings) over that period is precisely what you don’t want. In this situation, it may make more sense to choose investments that can offer higher returns, even if they may also deliver short-term losses.

Another important aspect of investment is knowing how to divide up your assets. This is the ‘lots of eggs, lots of baskets’ rule. Work out how much money you need for daily living and emergencies, then see how much is left over. Some of this you may still want to keep in low-growth, easy-access accounts, but with the rest you can afford to be more adventurous. This is the portion of your assets that has the potential to earn you long-term returns.

Find out if investment is for you

So how do you work out the right amount of risk to take? The easiest way is to talk to an independent financial planner. One of the first things most financial planners will do with you is a risk assessment, to find out your ideal investment strategy. Many who consider themselves cautious people discover they can take far more risk; conversely, those with a more cavalier attitude may discover that they need to rein themselves in. By working out your own ‘risk tolerance’, you can venture into higher-risk investments without it posing a serious risk to your plans. In fact, taking on some risk may prove to be less risky – in the long term – than playing ‘safe’ with cash.

Wrapping up

Bank interest rates have been low for a number of years and the outlook is for this to continue if not worsen. Inflation is picking up and will eat away at your savings at an increasing rate. But don’t fret, there are things you can do now to make a bad situation better:

- Shop around for the best bank account paying the highest rate of interest.

- Keep an eye on your savings. Check your statements and keep things under review.

- Consider if you should take a little more risk with your money so that it can grow in real terms.

- Consider a system like our ‘Dynamic Cash Management’ approach to maximise your savings interest.

- Talk to us to discuss your options and get a proper financial plan for your savings.

This article is adapted from one that first appeared on Unbiased.

NorthStar Insights

Stay right up-to-date with the latest financial news, get expert insight and analysis and exclusive special offers to help you make the most of your money.

NorthStar Insights is the free email newsletter enjoyed by over 3,000 people across the UK. Subscribe now to never miss another update.

Latest Articles

Digital Ghosts: Don’t Let Your Online Finances Haunt Your Family After You’re Gone 23 June 2026

Digital Ghosts: Don’t Let Your Online Finances Haunt Your Family After You’re Gone 23 June 2026- What the World Cup Can Teach Us About Financial Planning 2 June 2026

- Raising Money-Smart Kids: Essential Tips for Financial Education at Every Age 12 May 2026

- The Stranger in Your Mirror: Why Your Brain Can’t Connect With Your Future Self (And How Financial Forecasting Can Help) 21 April 2026

- Are Your Pensions Fit for Purpose? The Eight Warning Signs to Watch Out For 30 March 2026

- Twenty Simple Ways to Give Your Finances a Thorough Spring Clean 10 March 2026

- How to Manage Your Parents’ Money Through Later Life 17 February 2026

- Don’t Be a Financial Dinosaur: Ten Outdated Money Habits to Ditch Today 27 January 2026

- Revealed: The Biggest Retirement Regrets and How to Make Sure You Avoid Them 6 January 2026

- Caught in the Middle: Essential Financial Strategies for the Sandwich Generation 16 December 2025

- Budget 2025: The Key Changes That Could Affect Your Finances 26 November 2025

- The True Cost of Christmas: What Brits Really Spend (and How to Cut Down Without Being Scrooge) 25 November 2025

Disclaimer

The content of this article is for information purposes only and does not constitute a personal financial recommendation. You should always speak to a regulated financial planner before taking financial advice. This article is intended for UK residents only. All information correct at time of publication.

Tag Cloud

Awards, Accreditations & Trade Associations

NorthStar is proud to be a member of the leading financial planning trade associations. Through a continued commitment to adhere to the highest professional standards and deliver exceptional service, NorthStar has received a number of awards and professional accreditations.